Miranda Burks, CFP®

Miranda Burks, CFP®

Throughout your marriage, you and your spouse or partner have likely talked — and reached decisions together — about the big choices in your life: whether to have children, your career paths, the kind of home to buy, and where to live. So why does the idea of discussing life after work and planning for retirement generate emotions from anxiety to excitement for the experiences ahead?

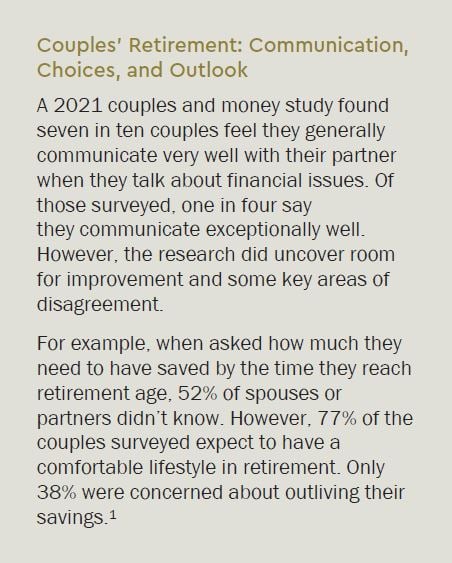

Perhaps it comes down to this: While most couples like to think they communicate with their loved ones about retirement issues, in reality they sense they may not be on the same page with respective retirement goals — making it difficult to open up about what they want later in life.

Do we share the same vision for retirement?

Clearly understanding what retirement will look like for each of you individually is just as important as how you view the future as a couple. You may be able to finish each other’s sentences at this point in your relationship, but you cannot read your spouse’s mind.

Start the conversation on a positive note — talk about the events, family milestones, and dreams you both agree on. Discuss what is most important to you and strive to understand what is most important to your loved one. Once you have shared your expectations, talk about how you can work as a couple to make your dreams a reality. Consider where your retirement goals follow a compatible path, and identity where your goals diverge.

Do we want to fully retire — and, if so, when?

Retirement today looks quite different than it did for prior generations, who generally left the workforce between ages 62 and 65. Nowadays, many individuals continue working in some capacity after traditional retirement — some out of financial necessity, others because they enjoy their careers or wish to start a new business.

According to a recent study of current and aspiring small business owners, 41% of people who own small businesses are baby boomers, and 13% are millennials.² Of those individuals surveyed, 61% of baby boomers said they would work through their retirement by choice, not necessity.² If you want to work after you retire, talk about the time commitment it will take to do what you would like.

Deciding when to retire may be the more complex part of the conversation, as your retirement may be longer than you think. According to the Social Security Administration, about one out of every three 65-year-olds today will live until at least age 90 — and one out of seven will live until at least age 95. Also, there is no “best age” for retiring. It is a personal decision based on a variety of factors: individual and family financial circumstances, cash needs, health situation, and family longevity — and when you want to start receiving Social Security benefits.³

Where do we want to retire?

Many couples find that without work and family obligations to tie them down to their location, retirement is time to finally explore new places either by moving or traveling. Some couples are choosing to move to a lower-cost state or country with a lower income tax rate or cost of living. Others are relocating because of climate change, inflation, health care costs, and rising crime rates. In fact, a 2018 study found that at least 12% of Americans have thought about living outside the U.S. when they retire. 4

You may think your spouse or partner will naturally feel this option is a good move if you do — however, he or she could be just as excited to settle into a quiet life in your home, age in place, and live near family and loved ones. Discuss your priorities and try to find a solution that works for both of you.

What kind of lifestyle do we want?

As we said earlier, 52% of couples don’t know how much money they will need to live comfortably in retirement. 1 A lot depends on what kind of lifestyle they plan on leading. Many couples also assume that building their nest egg stops at retirement. However, living a lavish lifestyle in a longer retirement means you may need to grow your assets for 30 years or more.

Being on the same page with your spouse or partner is critical to avoid surprises and to make the most of your financial situation. Couples should prepare for the very real possibility of a significant market decline during their golden years. Your spending habits may have to change, and one or both of you may need to consider part-time or self-employment.

What is our biggest worry?

When the couples surveyed were asked this question, three concerns rose to the top of the list:

- Having enough money saved for retirement (56% of millennials)

- Paying for health care in retirement (56%)

- Economic conditions out of their control (46%)1

Discussing your concerns as a couple now is a good start to determining how you would handle these situations in the future.

Do we have our affairs in order?

Generally, less than half of the adults in the U.S. have a will, according to numerous sources. Without this legal document in place, your spouse or partner may not know or be able to carry out your wishes in the event you pass away.

It is also important for spouses and partners to know where assets are stored and how to access accounts. Compile a comprehensive list of the contact and access information — names, phone numbers, account numbers, beneficiaries, and log in information, including passwords — for each asset you own, individually and jointly.

Finally, make it a point to discuss your retirement plans on a regular basis. Things change — giving the retirement portion of your life the proper attention now can help you negotiate compromises for disparities and prepare for an enjoyable retirement.

Next steps

While it may be tempting, don’t make any rash decisions to adjust your investment goals or change your portfolio without thoroughly weighing the pros and cons of doing so with your spouse, partner, or trusted family member. Have an open and honest discussion about what you want to change and why.

If you decide to adjust your goals or portfolio mix, we can’t over-emphasize the importance of working with a Financial Planner, Portfolio Manager, Wealth Consultant, or Private Client Advisor when making these important changes. Our financial professionals are experienced in helping couples adjust their investment goals, diversify their portfolios, and reduce their exposure to volatile asset classes and tax ramifications as they plan the retirement of their dreams.

Download the Article

¹“2021 Couples & Money Study,” Fidelity Investments Institutional Services Company, Inc., April 2021.

²Dragomir Simovic, “39 Entrepreneur Statistics You Need to Know in 2023,” , December 15, 2022.

³SocialSecurity.gov, “When to Start Receiving Retirement Benefits,” Publication No. 05-10147, January 2023.

4Laura Kiniry, “How to Retire Abroad—According to Those Who Have Done It,” Conde Nast Traveler, October 5, 2022.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP® and CERTIFIED FINANCIAL PLANNER™ in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

The opinions and other information in the commentary are provided as of March 15, 2023. This summary is intended to provide general information only, and may be of value to the reader and audience.

This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Past Performance is not a guarantee of future results. Diversification does not guarantee a profit or protect against all risk.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.