Koji Watanabe, CFP®, Financial Planning Manager

Koji Watanabe, CFP®, Financial Planning Manager

-

They don’t have the luxury of time on their side for their portfolios to recover from large or extended market downturns — younger adults investing for decades in the future have many more years and market cycles to recoup their losses and rebuild their portfolios.

-

For many pre-retirees and retirees, their investments provide a source of income to spend on daily living expenses and support their lifestyle. Younger adults are in more of a work-earn-save mindset with their investing habits.

Defining risk tolerance

In a nutshell, risk tolerance boils down to how well you’re able to handle volatility in your investment portfolio, which includes:

-

Dealing with uncertainty and coping with potential declines in the value of your portfolio’s assets.

-

Educating yourself about the investment option under consideration (because visualizing a loss may be much more than how that loss looks and feels if and when it becomes a reality).

-

Understanding that an investment is not a “loss” until it is liquidated.

-

Realizing a decline in value may be just part of the path to achieving higher value over the long term.

-

Quantifying the potential loss to help you put it into perspective and be more comfortable with the downside risk.

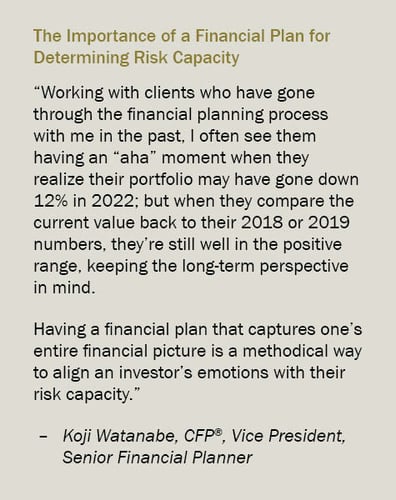

Overall, risk tolerance really does equate to understanding what your risk capacity is. For example, if the math says you can still achieve all of your goals despite losing $25,000 or seeing a 20% decline in your portfolio, it can add valuable peace of mind and comfort to the equation.

How to determine your risk tolerance

The following questions are designed to help your financial professional determine your risk tolerance when making an investment decision — you may want to jot down some notes to prepare for your conversation.

-

What are your goals with the portfolio, and how else might you achieve them should the portfolio not perform as expected?

-

What is your time horizon (e.g., years until retirement)? Generally, the longer the time horizon, the more options you have to choose from and volatility you should be able to withstand.

-

How does a particular investment fit into your overall net worth?

-

How well do you understand the mechanics of the investment vehicle(s) you’re considering?

-

What other sources of income do you have as alternatives?

-

How would you react in hypothetical scenarios (e.g., your $1,000,000 portfolio quickly declines to $850,000)?

When risk tolerance doesn’t align with risk capacity

Undoubtedly, your emotions and peace of mind are important aspects of the equation. Often investors are forced to deal with the emotions around making investment decisions when their risk tolerance doesn’t match up with the amount of risk they can actually afford.

If investment decisions are making you anxious and keeping you up at night, then it’s time for a change. Ask yourself this: “What level of decline or volatility makes me nervous and triggers my stress?” Answering the question honestly can help draw the lines and set boundaries to determine which investment options should be considered and adjusted.

Steps to de-risk your portfolio

In an ideal setting, you should not have to de-risk or make portfolio changes in response to market volatility. These circumstances should have been factored into consideration prior to implementing your investment strategy. Still, it can be a challenge when market volatility hits right at the time you were expecting to access your investments for important life events (e.g., paying for a child’s upcoming college tuition, buying a vacation home, or starting a retirement business).

During extended periods of market stress, there are steps you may want to consider to de-risk your portfolio that will help you stay on track with your financial goals.

With your Portfolio Manager or financial professional, thoroughly weigh the pros and cons of making any changes to your portfolio that alter your original investment plan. As tempting it may be, don’t make any rash decisions. As an extreme example, liquidating an all-stock portfolio to cash to avoid the current volatility would come with unintended consequences: transactional costs, trigger unnecessary taxes, and missing out on the potential upswing in the market. Always keep in mind what you’re experiencing is likely just a short segment of a much longer timeframe.

Next steps

When it comes to determining your risk tolerance, we can’t emphasize enough the importance of working with a Financial Planner, Wealth Management Consultant, or Private Client Advisor. Particularly during turbulent times in the market, our financial professionals are experienced in helping clients diversify their portfolios and reduce exposure to more volatile asset classes.

Contact Commerce Trust today. Discover firsthand how our team can offer guidance with your investment portfolio and implement a wide range of solutions to help fulfill all your financial services needs.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the certification marks CFP® and CERTIFIED FINANCIAL PLANNER™ in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Past performance is not a guarantee of future results, and the opinions and other information in the commentary are provided as of January 18, 2023. This summary is intended to provide general information only, and may be of value to the reader and audience.

Diversification does not guarantee a profit or protect against all risk. This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Commerce Trust is a division of Commerce Bank.

INVESTMENT PRODUCTS: NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE