Scott Colbert

Scott Colbert

The U.S. housing market has been impacted by several factors including elevated interest rates, constrained supply, and deteriorating affordability. These impacts are reshaping both household finances and broader economic growth. The housing market’s influence extends far beyond construction activity, affecting inflation, consumer spending, and long-term wealth formation.

An imbalanced market

Today’s housing dynamics are influenced by a persistent supply-demand imbalance. The U.S. remains structurally underbuilt, with an estimated shortfall of three to five million housing units. Yet despite this unmet demand, home sales remain subdued, largely due to affordability constraints rather than lack of interest from homebuyers.

New home construction represents about 3.6% of GDP (gross domestic product), near a historical low, underscoring depressed sales activity. Existing homeowners are reluctant to sell because they are anchored to significantly lower mortgage interest rates than those currently available. As a result, existing home inventory remains tight, with only about three to four months of supply, which is below historical average of five to six months’ supply.

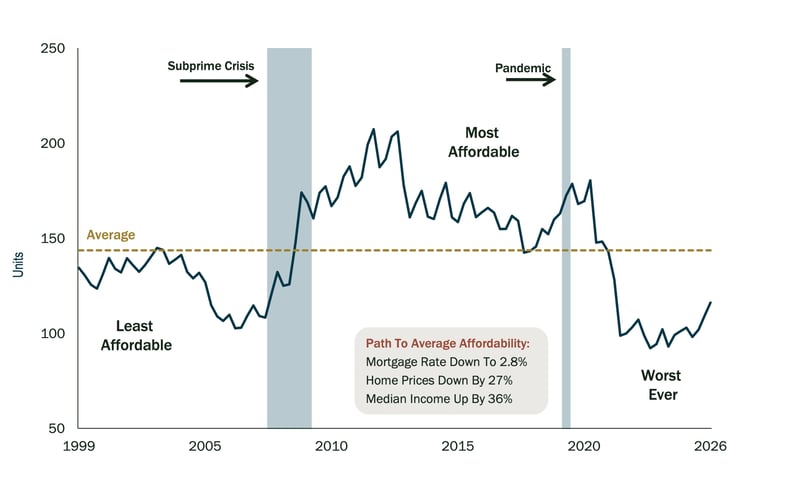

Housing Affordability Since 1999

Weakest housing affordability in 25 years sees steep path to improvement

Source: Bloomberg; Federal Reserve Bank of New York; U.S. Census Bureau

Affordability, measured by the gap between home prices and household incomes, remains the defining challenge. Over the past six years, median home prices have surged while median household incomes have only increased moderately.

Higher borrowing costs strain the situation further. Mortgage rates have roughly doubled, from 3.25% pre-pandemic to about 6.4% today, dramatically increasing monthly payments.

For first-time buyers, the gap is even more pronounced. With average renter incomes closer to $70,000, many prospective buyers are effectively priced out of the market. This affordability gap not only limits homeownership but also has broader implications for wealth accumulation, as housing remains a primary asset for most U.S. households.

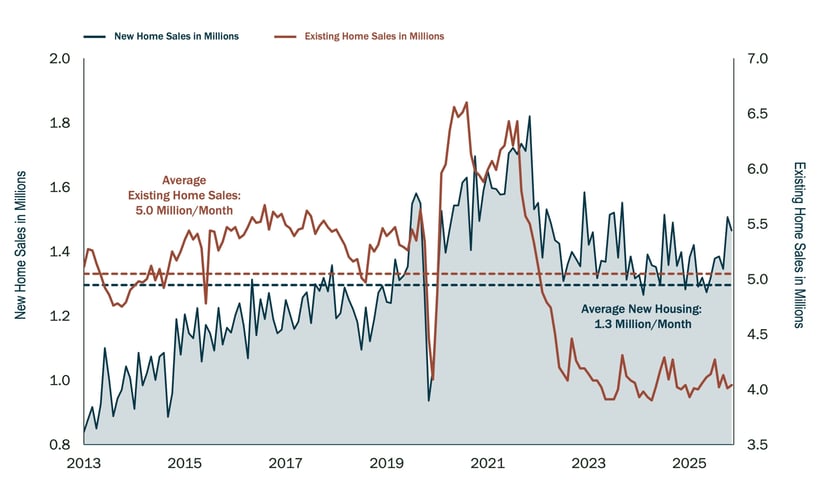

New Home Sales versus Existing Home Sales

New home sales outpace existing home sales as inventory reaches historic lows

Source: Bloomberg; Federal Reserve Bank of New York; U.S. Census Bureau

Housing’s role in inflation

Housing is also the single largest component of inflation. It accounts for roughly 34–35% of the Consumer Price Index (CPI), encompassing rents, owners’ equivalent rent which is an estimate of how much a homeowner would pay to rent their own home if they were renting, and related housing costs.

Despite prolonged spikes in energy prices, housing trends are likely to exert a more significant influence on inflation going forward. As home price appreciation and rent growth slow, housing-related inflation has begun to cool, running around 3.4%1, below the headline CPI of 3.8%.

This divergence highlights an important dynamic, while energy price shocks are highly visible, their direct weight in inflation can be relatively small, around 3%, whereas housing has historically exerted a much larger and more persistent influence.

Interest rates remain elevated

Looking ahead, the interest rate environment remains a critical variable. Market expectations suggest rates could remain elevated for an extended period, as expectations for a Federal Reserve interest rate cut diminish with rising inflation. With the addition of geopolitical uncertainty and energy price volatility, monetary policy is expected to remain restrictive.

Higher rates disproportionately impact housing due to its sensitivity to financing costs. Elevated borrowing expenses continue to suppress both demand, by reducing affordability, and supply, by discouraging development. As a result, housing activity remains cyclical and vulnerable in the current environment.

Regional divergence and structural shifts

Not all regions are experiencing the same housing pressures. The Midwest in particular has emerged as relatively resilient, benefiting from lower home prices and increased investment tied to data center construction. Lower electricity costs and more moderate price appreciation have helped sustain home building, buying, and selling in this region even as other parts of the country slow.

Across the U.S., broader construction trends are shifting. While data center development remains robust, traditional segments like office construction, apartment development, and healthcare facilities have slowed materially under the weight of higher rates and changing economic incentives.

Looking ahead

Housing’s importance extends beyond its direct contribution to GDP. When accounting for all related expenditures of rent, mortgage payments, insurance, and household goods; housing represents approximately 16–17% of total economic activity, rivaling the healthcare sector in scale.

Housing plays a critical role in how monetary policy affects the broader economy. Elevated interest rates are cooling home price growth and, by extension, inflation, but at the cost of reduced homeowner mobility, weaker construction activity, and constrained consumer spending.

The path to restoring housing affordability is challenging and likely requires a combination of factors including, rising incomes, stabilizing home prices, and eventually lower interest rates. Until these forces align, the housing market is likely to remain constrained, defined by limited inventory, subdued transaction volumes, and continued pressure on first-time homebuyers.

For investors and policymakers alike, the takeaway is clear. Housing is not just a sector, it continues to be a foundational pillar of the U.S. economy. The evolution of the housing sector in the coming years will play a decisive role in shaping inflation, growth, and financial stability.

1As of May 2026, Consumer Price Index shelter component

Past performance is no guarantee of future results, and the opinions and other information in the commentary are as of July 8, 2026. This summary is intended to provide general information only and is reflective of the opinions of Commerce Trust. This material is not a recommendation of any particular security, is not based on any particular financial situation or need and is not intended to replace the advice of a qualified attorney, tax advisor or investment professional.

Diversification does not guarantee a profit or protect against all risk. Commerce Trust does not provide tax advice or legal advice to customers. Consult a tax specialist regarding tax implications related to any product and specific financial situation. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Commerce Trust is a division of Commerce Bank

Investment Products: Not FDIC Insured | May Lose Value | No Bank Guarantee