Kelly Jernigan J.D., CFA® Senior Vice President, Director, Family Wealth Strategy

Kelly Jernigan J.D., CFA® Senior Vice President, Director, Family Wealth Strategy

In recent years, companies have been going public at a slower rate with more choosing to stay private for longer. In addition to fewer public companies to invest in, more investments are flowing into passive funds. Passive investments provide less visibility into individual stock prices and valuation, rather just showing beta or the level of risk relative to the broader market.

In a market like this, active funds with active managers may find opportunities to outperform the market. We will take a deeper look at how the markets arrived at this point and whether a shift is on the horizon.

Companies remaining private for longer

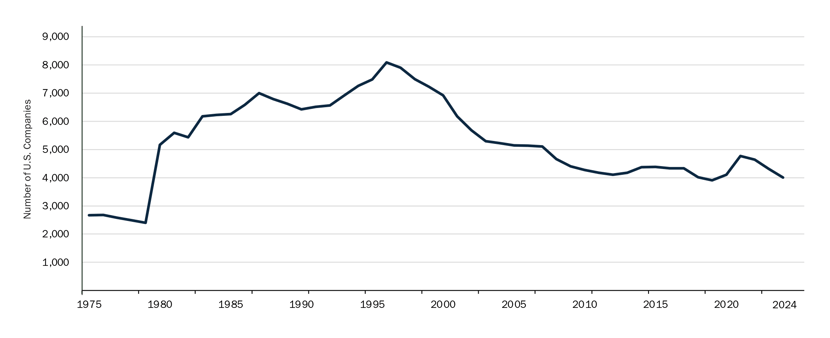

Primary markets, where companies are sold to the public for the first time through an initial public offering (IPO), are shifting as more companies opt to remain private. Over the last thirty years, the total number of publicly traded U.S. companies has declined. After peaking at 8,090 in 1996, the number of publicly listed companies in the U.S. declined to 4,010 by 2024.1 During this same period, private markets have flourished.

Total Listed Domestic Companies

Number of public companies declining since 1990s peak

Source: World Bank.

Public investors’ access to growth delayed

By remaining private, companies have more control and lower costs in some key areas. For example, private companies do not have the same oversight as public companies, so they can avoid hiring outside auditors and have lower compliance costs.

IPOs are no longer needed to raise funds. Companies can raise capital without going public through acquisition either by a public company or private equity. In the past, private equity investors were able to exit investments in companies through IPOs after a 10-to-12-year cycle. Now, private equity may launch successor funds or make private-to-private deals on the secondary market.

Private companies can focus on long-term innovation and employment rather than short-term stock performance, but there are risks to staying private. Private companies do not have to disclose financials, there is less investor insight into their performance, governance, and management. If too many firms avoid public markets, the lack of transparency and accountability may reduce market efficiency and complicate the valuation of companies.

As a result, as fewer companies go public early, public investors have access to fewer early-stage growth opportunities and often gain access only after a company’s peak growth stage.

High frequency trading disconnects from fundamentals

High frequency trading (HFT) has also impacted public markets. HFT is performed with advanced computer software and sophisticated algorithms to execute vast numbers of orders in fractions of a second. The algorithms rapidly analyze numerous markets and respond to varying market conditions to execute trades efficiently. Having the fastest execution speeds allows traders and financial institutions to capitalize on minimal price discrepancies for higher profitability. Although the profits are small per trade, traders can profit by making millions of trades each day. However, because HFT relies on ultra-fast computers and networks, any malfunctions can potentially lead to losses for investors within milliseconds. If markets are stressed, HFT may withdraw from the markets, losing liquidity and increasing price swings. Price swings become driven by automated strategies, not fundamentals.

HFT can drive price swings based on algorithmic strategies rather than underlying business fundamentals, making markets more volatile and less predictable.

Third markets reduce transparency as well

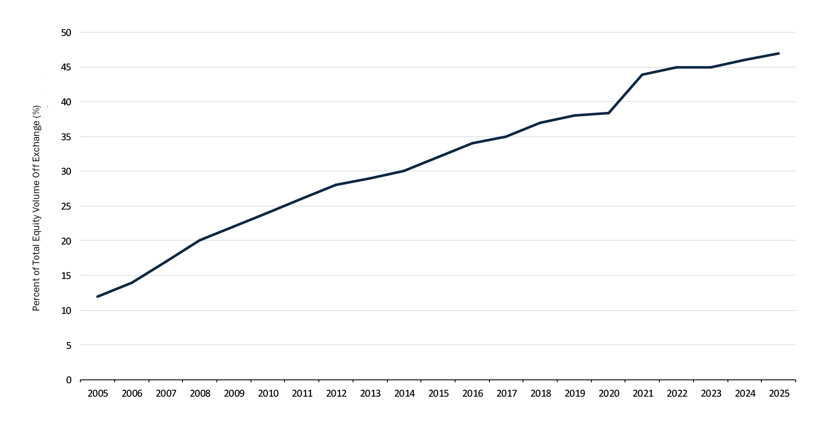

Third markets, or private to private transactions of public market securities, impact public markets as well. Dark pools are designed for trading large blocks of securities by institutional investors, such as hedge funds, pension funds, and active manager mutual funds away from the public eye. Dark pool trades happen privately and are not made public until the trades are final. Reduced transparency may benefit big investors but can leave retail investors at a disadvantage. In 2025, dark pool and off-exchange trading accounted for nearly 50% of total U.S. equity trading volume.

Off-Exchange Trading as Percentage of Total Equity Trading Volume

Dark pool trading now accounts for over half of all equity trading volume

Source: 2005, SEC Market Structure Report; 2015 FINRA ATS Transparency Data; 2022 Bloomberg Market Data; 2025 Reuters Trading Volume Report.

Dark pools help active managers by minimizing the market impact of trades, prevent HFT based on advanced information and can help customize trading execution. Index funds may use dark pools when rebalancing, but less frequently than active managers. Reduced market impact, improved price execution, and anonymity benefit institutional traders. But reduced transparency in pricing and market fragmentation poses a greater risk for investors.

More IPOs may be coming in 2026

Market conditions may be shifting toward a friendlier IPO market. Interest rate hikes in 2022 turned off some investors and IPO markets cooled. But with lower interest rates, increased liquidity, and higher valuations, the markets are beginning to open again, especially for non-technology companies. In late 2025, medical supply company Medline Industries went public at $7.2 billion and has experienced strong trading since. More traditional companies, rather than super fast-growing technology companies, may be an attractive way for investors to diversify.

The Commerce Trust investment approach

At Commerce Trust, we believe long-term investors should focus on fundamentals and avoid reacting to short-term volatility. We remain diligent in exploring opportunities and evaluating risks inside financial markets and have portfolios positioned with a balanced, neutral posture.

1https://data360.worldbank.org/en/indicator/WB_WDI_CM_MKT_LDOM_NO?view=trend&country=USA&minYear=1980

The Chartered Financial Analyst® (CFA®) Charter is a designation granted by CFA Institute to individuals who have satisfied certain requirements, including completion of the CFA Program, and required years of acceptable work experience. Registered marks are the property of CFA Institute.

Past performance is no guarantee of future results, and the opinions and other information in the commentary are as of March 18, 2026. This summary is intended to provide general information only and is reflective of the opinions of Commerce Trust. This material is not a recommendation of any particular security, is not based on any particular financial situation or need and is not intended to replace the advice of a qualified attorney, tax advisor or investment professional.

Diversification does not guarantee a profit or protect against all risk. Commerce Trust does not provide tax advice or legal advice to customers. Consult a tax specialist regarding tax implications related to any product and specific financial situation. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Alternative Investments often carry additional risk considerations and may involve significant losses, periods of extreme volatility, and lack of liquidity. These investments, in general, are not suitable for all investors. Additionally, certain alternative investments may require investors to be accredited or qualified investors, which have defined minimum asset requirements.

Commerce Trust is a division of Commerce Bank.

Investment Products: Not FDIC Insured | May Lose Value | No Bank Guarantee