Christopher A. Smith, Vice President, Private Client Advisor

Christopher A. Smith, Vice President, Private Client Advisor

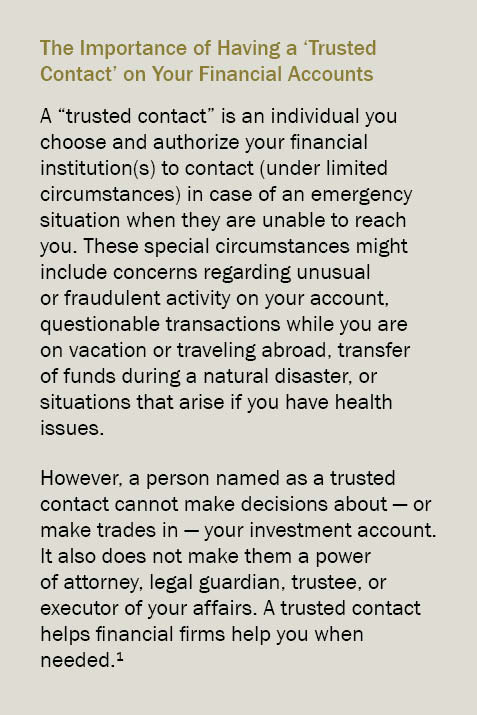

There are a number of ways financial institutions strive to safeguard your hard-earned money. One of the most popular practices encouraged by banks, credit unions, and brokerage firms is to allow you to choose one or more trusted contacts whom they can reach out to in case of suspected fraud or other emergencies regarding your accounts when they can’t contact you.

It’s just one more way the institutions you do business with can help protect financial well-being and independence for you and vulnerable elderly adults.

How to set up a trusted contact on an account

Before you decide to set up a trusted contact on an account, it’s important to fully understand the ramifications of this decision. The main reason you’re choosing a trusted contact is because you believe that person will act in your best interest and assist the financial institution in protecting you and your assets.

Decide who would be the best fit for this job. Choose someone you trust — a relative, friend, attorney, or another person who is not only reliable but also will do what’s best for you under any circumstance. You may want to select more than one individual to include on a list of trusted contacts. (In case the first person on your list is not available, your financial institution can reach out to other trusted contacts you have selected.)

Visit your financial institutions. Visit each financial institution where you have an account and ask them go over their trusted contact policy. Request a copy of their policy, make sure you understand what the guidelines are, and have them answer any questions you may have before providing information regarding your trusted contact(s).

Verify the information your bank or brokerage firm is allowed to share with a trusted contact. For example, if you’re uncomfortable with the scope of what will be discussed with a truhttps://www.commercetrustcompany.com/research-and-insights/videos/whats-behind-the-equities-rallysted contact, ask if you can limit the information that will be shared. If you have concerns about privacy matters, family relationships, or money issues, this is the time to inform your banking or brokerage professional.

Ask your financial institution(s) what process they follow if they suspect your trusted contact may be involved in fraudulent activity on your account. No one likes to think a family member or close acquaintance would try to take advantage of their financial situation, but it happens. (That’s why it’s a good idea to have more than one trusted contact in case your bank or brokerage firm suspects your first contact may be involved in criminal activity.) The Consumer Financial Protection Bureau also suggests it may be wise to name a trusted contact who doesn’t have control over your finances or ownership interest in your accounts.²

Contact your financial institution(s) immediately if you decide to change a trusted contact. If for any reason you decide you want to remove your trusted contact or switch the responsibility to another person, contact your bank, credit union, or brokerage firm immediately. Tell them they no longer have your permission to share any information with that particular individual. Most likely you’ll have to sign documentation to that effect.

We can help protect your assets

One of the most effective tools to help protect the assets in your accounts — and your financial independence — is to allow us to alert a trusted contact in an emergency should a suspicious situation occur. Not only does this help you maintain control of your finances, it also may keep you from becoming a victim of financial exploitation. Commerce Trust is here to answer your questions regarding trusted contacts and explain the process for setting up this added step for safety and security protection on your accounts. Call today for more information.

¹FINRA, “Establishing a Trusted Contact,” https://www.finra.org/investors/learn-to-invest/brokerage-accounts/establish-trusted-contact, accessed October 6, 2022.

²Consumer Financial Protection Bureau, “Choosing a trusted contact person can help you protect your money,”

https://files.consumerfinance.gov/f/documents/cfpb_trusted-contacts-consumers_2021-11.pdf

The opinions and other information in the commentary are provided as of November 2, 2022. This summary is intended to provide general information only, and may be of value to the reader and audience.

This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Commerce Trust is a division of Commerce Bank.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

Why Older Adults Are Targets For Financial Fraud

How to set up a trusted contact on an account

Before you decide to set up a trusted contact on an account, it’s important to fully understand the ramifications of this decision. The main reason you’re choosing a trusted contact is because you believe that person will act in your best interest and assist the financial institution in protecting you and your assets.

Decide who would be the best fit for this job. Choose someone you trust — a relative, friend, attorney, or another person who is not only reliable but also will do what’s best for you under any circumstance. You may want to select more than one individual to include on a list of trusted contacts. (In case the first person on your list is not available, your financial institution can reach out to other trusted contacts you have selected.)

Visit your financial institutions. Visit each financial institution where you have an account and ask them go over their trusted contact policy. Request a copy of their policy, make sure you understand what the guidelines are, and have them answer any questions you may have before providing information regarding your trusted contact(s).

Verify the information your bank or brokerage firm is allowed to share with a trusted contact. For example, if you’re uncomfortable with the scope of what will be discussed with a truhttps://www.commercetrustcompany.com/research-and-insights/videos/whats-behind-the-equities-rallysted contact, ask if you can limit the information that will be shared. If you have concerns about privacy matters, family relationships, or money issues, this is the time to inform your banking or brokerage professional.

Ask your financial institution(s) what process they follow if they suspect your trusted contact may be involved in fraudulent activity on your account. No one likes to think a family member or close acquaintance would try to take advantage of their financial situation, but it happens. (That’s why it’s a good idea to have more than one trusted contact in case your bank or brokerage firm suspects your first contact may be involved in criminal activity.) The Consumer Financial Protection Bureau also suggests it may be wise to name a trusted contact who doesn’t have control over your finances or ownership interest in your accounts.²

Contact your financial institution(s) immediately if you decide to change a trusted contact. If for any reason you decide you want to remove your trusted contact or switch the responsibility to another person, contact your bank, credit union, or brokerage firm immediately. Tell them they no longer have your permission to share any information with that particular individual. Most likely you’ll have to sign documentation to that effect.

We can help protect your assets

One of the most effective tools to help protect the assets in your accounts — and your financial independence — is to allow us to alert a trusted contact in an emergency should a suspicious situation occur. Not only does this help you maintain control of your finances, it also may keep you from becoming a victim of financial exploitation. Commerce Trust is here to answer your questions regarding trusted contacts and explain the process for setting up this added step for safety and security protection on your accounts. Call today for more information.

¹FINRA, “Establishing a Trusted Contact,” https://www.finra.org/investors/learn-to-invest/brokerage-accounts/establish-trusted-contact, accessed October 6, 2022.

²Consumer Financial Protection Bureau, “Choosing a trusted contact person can help you protect your money,”

https://files.consumerfinance.gov/f/documents/cfpb_trusted-contacts-consumers_2021-11.pdf

The opinions and other information in the commentary are provided as of November 2, 2022. This summary is intended to provide general information only, and may be of value to the reader and audience.

This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Commerce Trust is a division of Commerce Bank.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE