4 min read

Perhaps you have been thinking about selling your business. What if you could sell your business in a way that provides an income stream for you or a loved one, but also defers capital gain tax, and benefits your favorite charities? A charitable remainder trust (CRT) could be just the strategy you are looking for to accomplish these goals.

It is important to state upfront that CRTs are complex estate planning tools that come in many shapes and sizes. Numerous factors must be considered to determine which type of CRT best fits your needs.

Bottom line, the basics you should know about CRTs:

How does a CRT work?

To create a CRT, you (the donor) must first execute a trust. The trust will set forth the type and amount of the distribution (e.g., a fixed dollar amount or a fixed percentage amount of the trust), as well as to whom and for what duration benefits will be paid. The trust will also set forth the charity or charities to receive the remaining trust assets at the end of the defined period. Although CRTs are irrevocable, you may retain the right to change the charitable beneficiary or beneficiaries.

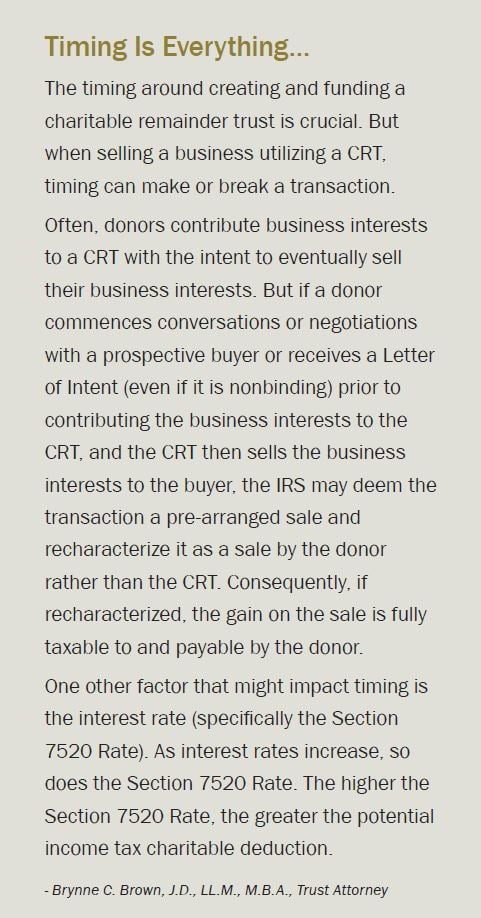

Once the trust is executed, you (the donor) will fund the CRT with cash and/or other non-cash assets. You can fund the CRT with your business interests (note, the timing of contribution of your business interests and the sale of those business interests is very important). A qualified appraisal by a qualified appraiser is required for any non-cash assets contributed to the CRT. A qualified appraisal is especially important if you are funding the CRT with your business interests.

Once the CRT is funded, you (the donor) or other non-charitable beneficiary (e.g., spouse, partner, child, etc.) will receive the distribution specified in the trust for the defined period. At the end of the defined period, the remaining value of the CRT is distributed to the charitable beneficiary or beneficiaries.

Okay, but what about taxes?

The creation and funding of a CRT has significant income and estate tax implications to you (the donor).

You (the donor) must file a U.S. Gift Tax Return (IRS Form 709) for all assets contributed to the CRT. The qualified appraisal of the non-cash assets is critical for purposes of filing IRS Form 709. The assets contributed to a CRT (and validly detailed on IRS Form 709) are removed from your estate, so no estate taxes are due on those assets at your death.

The tax year during which the assets are contributed to the CRT, you (the donor) may be able to take an income tax charitable deduction on your U.S. Individual Income Tax Return (IRS Form 1040) based on the present value of the charitable remainder interest. The charitable remainder interest must equal at least 10% of the initial fair market value of the assets contributed; otherwise, the CRT will fail. The present value of the charitable remainder interest is measured using an actuarial formula that accounts for the defined period of the CRT and the “Section 7520 Rate” published monthly by the IRS. Note, however, the income tax charitable deduction is subject to prescribed Adjusted

Gross Income (AGI) limitations.

Also, the IRS can deny an income tax charitable deduction if the appraisal on the non-cash assets contributed to the CRT does not comply with IRS guidelines for a qualified appraisal or if no appraisal is obtained.

If utilizing a CRT to sell your business, once the business is sold, the CRT is not subject to capital gains tax. You or the other non-charitable beneficiary will pay income tax on the income distributed from the CRT, which is taxed as capital gains or ordinary income depending on the type of income distributed, and distributions of principal are tax-free.

After a CRT is created and funded, the CRT is treated as a private foundation for federal tax purposes (unless an exception applies). Private foundations are subject to strict rules and restrictions prescribed by the Internal Revenue Code.

Pros and Cons of a CRT

The following are some of the pros and cons that should be carefully weighed and discussed with your estate planning attorney and tax advisor.

It is important to state upfront that CRTs are complex estate planning tools that come in many shapes and sizes. Numerous factors must be considered to determine which type of CRT best fits your needs.

Bottom line, the basics you should know about CRTs:

- A CRT is an irrevocable trust used for tax planning and philanthropic purposes.

- You (the donor) would create a CRT to provide an income stream for you or other non-charitable beneficiary (e.g.,

spouse, partner, child, etc.) for a fixed number of years (not more than 20) or for the life of the named beneficiary. After the defined period has lapsed, the CRT goes on to benefit one or more designated charities. - CRTs can be useful vehicles to sell your business interests, but you (the donor) should be aware of a variety of impacts — tax and otherwise — in contributing to and then selling said business interests through a CRT.

How does a CRT work?

To create a CRT, you (the donor) must first execute a trust. The trust will set forth the type and amount of the distribution (e.g., a fixed dollar amount or a fixed percentage amount of the trust), as well as to whom and for what duration benefits will be paid. The trust will also set forth the charity or charities to receive the remaining trust assets at the end of the defined period. Although CRTs are irrevocable, you may retain the right to change the charitable beneficiary or beneficiaries.

Once the trust is executed, you (the donor) will fund the CRT with cash and/or other non-cash assets. You can fund the CRT with your business interests (note, the timing of contribution of your business interests and the sale of those business interests is very important). A qualified appraisal by a qualified appraiser is required for any non-cash assets contributed to the CRT. A qualified appraisal is especially important if you are funding the CRT with your business interests.

Once the CRT is funded, you (the donor) or other non-charitable beneficiary (e.g., spouse, partner, child, etc.) will receive the distribution specified in the trust for the defined period. At the end of the defined period, the remaining value of the CRT is distributed to the charitable beneficiary or beneficiaries.

Okay, but what about taxes?

The creation and funding of a CRT has significant income and estate tax implications to you (the donor).

You (the donor) must file a U.S. Gift Tax Return (IRS Form 709) for all assets contributed to the CRT. The qualified appraisal of the non-cash assets is critical for purposes of filing IRS Form 709. The assets contributed to a CRT (and validly detailed on IRS Form 709) are removed from your estate, so no estate taxes are due on those assets at your death.

The tax year during which the assets are contributed to the CRT, you (the donor) may be able to take an income tax charitable deduction on your U.S. Individual Income Tax Return (IRS Form 1040) based on the present value of the charitable remainder interest. The charitable remainder interest must equal at least 10% of the initial fair market value of the assets contributed; otherwise, the CRT will fail. The present value of the charitable remainder interest is measured using an actuarial formula that accounts for the defined period of the CRT and the “Section 7520 Rate” published monthly by the IRS. Note, however, the income tax charitable deduction is subject to prescribed Adjusted

Gross Income (AGI) limitations.

Also, the IRS can deny an income tax charitable deduction if the appraisal on the non-cash assets contributed to the CRT does not comply with IRS guidelines for a qualified appraisal or if no appraisal is obtained.

If utilizing a CRT to sell your business, once the business is sold, the CRT is not subject to capital gains tax. You or the other non-charitable beneficiary will pay income tax on the income distributed from the CRT, which is taxed as capital gains or ordinary income depending on the type of income distributed, and distributions of principal are tax-free.

After a CRT is created and funded, the CRT is treated as a private foundation for federal tax purposes (unless an exception applies). Private foundations are subject to strict rules and restrictions prescribed by the Internal Revenue Code.

Pros and Cons of a CRT

The following are some of the pros and cons that should be carefully weighed and discussed with your estate planning attorney and tax advisor.

Pros

- Current reduction in income taxes and future reduction (possible elimination) of estate taxes

- Current income stream for a period of years or for life for you or other non-charitable beneficiaries

- Future benefit to one or more charities of your choice

- Reduction of capital gains upon sale of assets, specifically low basis, highly appreciated assets, from the CRT

- Limitation of income tax charitable deductions because of AGI limitations

- The income generated inside the CRT is generally exempt from income tax, but the income distributed from the CRT to the donor or other non-charitable beneficiary is income taxable to such recipient

- Loss of control over the assets contributed to the CRT, as CRTs are irrevocable

- The appraisal process for non-cash assets can be costly and time-consuming

- Private foundation rules and restrictions and other tax traps

This is a lot of information on CRTs to absorb. However, it only scratches the surface of what you need to consider if you are contemplating selling your business utilizing a CRT.

Our team of Private Client Advisors, alongside your estate planning attorney and tax advisor, can help you explore the variety of options available to you and assist you with making educated decisions based on your goals and unique financial situation. Contact Commerce Trust today.

Download the Article

The opinions and other information in the commentary are provided as of August 30, 2023. This summary is intended to provide general information only, and may be of value to the reader and audience.

This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Commerce does not provide tax advice to customers unless engaged to do so. Consult a tax specialist regarding tax implications related to any product and specific financial situation. Commerce does not provide legal advice to its customers. Consult an attorney for legal advice, including drafting and execution of estate planning documents.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

INVESTMENT PRODUCTS: NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

The opinions and other information in the commentary are provided as of August 30, 2023. This summary is intended to provide general information only, and may be of value to the reader and audience.

This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Commerce does not provide tax advice to customers unless engaged to do so. Consult a tax specialist regarding tax implications related to any product and specific financial situation. Commerce does not provide legal advice to its customers. Consult an attorney for legal advice, including drafting and execution of estate planning documents.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

INVESTMENT PRODUCTS: NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE