Hugo Figueira, Private Banker

Hugo Figueira, Private Banker

It comes as no surprise that reports of financial crimes against elderly adults are on the rise. Each year, more than 3.5 million seniors are victims of financial exploitation. Fraudsters swindle vulnerable individuals out of more than $3 billion annually, and seniors can suffer up to an average of $34,200 with some types of fraud.¹ Consumer and government agencies fear these numbers are much higher, since many victimized adults are too embarrassed or afraid to report the crimes.

The truth of the matter is scammers can target people of any age — even you. Individuals over the age of 60 are often the most vulnerable, and victims over the age of 80 tend to suffer higher financial losses.¹ Elderly adults are easy prey for family members, domestic employees, caregivers — even complete strangers — who exploit them for personal gain.

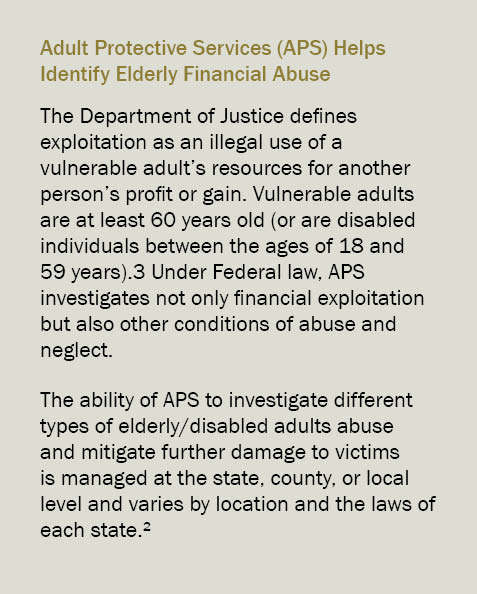

Fortunately, in addition to law enforcement capabilities for investigation and prosecution of violators, there are government resources available to elderly victims of financial exploitation, abuse, and neglect. One of the most effective resources is Adult Protective Services (APS), managed by the Consumer Financial Protection Bureau.²

While voluntary reporting to government agencies is highly encouraged to prevent and mitigate damage from elder abuse, there are also a number of ways financial institutions monitor and identify unusual activity for their customers and clients. The following are some of the situations and examples they watch out for — and you should too, to protect yourself and your vulnerable loved ones.

Red flags for elderly financial abuse

Check activity

-

Handwriting inconsistencies. It’s common for an older adult to sign a blank check and hand it over to a trusted individual to pay a bill. An exploiter (often someone who has a close relationship to the elderly person) might make the check payable to himself, sometimes to pay one of his obligations. The signature on the check matches the financial institution’s records, but the handwriting for the rest of the information on the check will not.

-

Alterations. An exploiter might change the payee on a check (for example, I.R.S. to I.R. Stewart), erase and rewrite the party on the payee line, and modify the dollar amount.

-

Out-of-sequence check numbers. A fraudster may steal a booklet in a box of checks for personal use while the victim is still working on the current booklet.

-

Large amounts or overly frequent checks to individuals. Often this is a sign the elderly victim may have been misled or the checks were stolen.

-

Returned deposited items and/or overdraft activity on an account. A fraudster takes advantage of an older person’s great track record to abuse the account which will suddenly start to be hit with returned checks and overdraft fees.

-

Missing or mismatched signatures. Missing signatures or signatures that don’t match on an elderly client’s checks are often signs of fraudulent activity by an exploiter.

Electronic and ACH transactions

-

Excess subscriptions or duplicate utilities. A caregiver might take advantage of a trusting individual by paying personal bills from an elderly person’s financial accounts.

-

PayPal or similar payment app. This is a common way for a fraudster to hide theft as a potentially legitimate transaction.

-

Credit card payments in large amounts. This is particularly alarming to financial institutions when they notice large duplicate payments from a senior to the same card company.

-

Large purchases, particularly online. Elderly persons may never see large purchases or recognize the transactions if they don’t check their financial accounts on a monthly basis.

-

Internal transfers to joint accounts. This type of financial fraud is common when family members are involved in the day-to-day care of elderly or disabled relatives (especially when they all live at the same address).

Online bill payments

-

Payments to individuals. Most elderly people exclusively pay companies or utilities via this account service — but payments to individuals are not the norm.

-

Bill payments to outside personal footprint or new institutions. Older adults tend to do business locally and are creatures of habit. Random bill payments to parties outside their personal footprint or new and unknown institutions should be suspect.

Credit cards

-

Requesting new cards or authorized users. Bank clients don’t always realize they are fully responsible for any financial transactions their authorized users charge. Elderly individuals requesting new or additional cards or authorizing other users on their accounts could be a red flag.

-

Balance transfers. Often the balance transfers involve the exploiter — another good reason to check financial records of elderly loved ones on a regular basis.

-

Online recurring bills and e-subscriptions. Often these types of card charges are small amounts and easy to overlook. However, over a period of time the costs for digital services and items can quickly add up (e.g., online shopping, streaming subscriptions, digital newspapers and magazines, videos and movies, etc.). Make sure the bills and subscriptions benefit an elderly loved one and not someone else.

In-person transactions

-

Large or numerous cash withdrawals. Watch for large or frequent cash withdrawals. Funds may be removed under coercion or deceitfully, and cash is hard to trace once misappropriated.

-

Co-signing or refinancing loans. These types of transactions may also be carried out under coercion or deceitfully.

-

Excessive ATM usage. ATMs allow for lesser scrutiny of transactions and minimal or no personal contact or interaction with a financial institution.

We can help

If you or a loved one is a victim of elderly financial fraud or abuse, Commerce Trust is here to help. When a crime is suspected, we have processes in place to gather evidence and report the evidence to the appropriate authorities. We will answer your questions regarding the safety and security of the affected accounts and explain next steps for protecting your assets. Call today for more information.

¹ Emma Rubin, Consumer Affairs, “Senior Financial Scams,” www.consumeraffairs.com/finance/elderly-financial-scam-statistics.html, updated February 17, 2022.

² Consumer Financial Protection Bureau, ”Adult Protective Services,” https://www.consumerfinance.gov/consumer-tools/educator-tools/resources-for-older-adults/elder-protection-networks/resources/adult-protective-services/’, accessed September 28, 2022.

3 Department of Justice, “Elder Abuse and Elder Financial Exploitation Statutes,” https://www.justice.gov/elderjustice/prosecutors/statutes, accessed October 20, 2022.

The opinions and other information in the commentary are provided as of November 2, 2022. This summary is intended to provide general information only, and may be of value to the reader and audience.

This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Commerce Trust is a division of Commerce Bank.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE