Mendy Diel

Mendy Diel

You’ve found your perfect getaway spot to spend your weekends, summer vacations, holidays and retirement with family and friends. Perhaps it’s a beach house, mountain cabin, ski condo or luxurious home in an upscale resort community. Or maybe you’re contemplating your next adventure in a place you’ve only read about or passed through once or twice. The big question is this: “Is now the time for you to buy a second home – not only for your family’s use and pleasure, but also for the enjoyment of renters who will help generate a source of additional income?” You’re not alone in considering the answer.

“Location, location, location”

It comes as no surprise that in some of the tightest markets across the country, well-priced homes in the most sought-after locations can sell within a few hours of going up for sale. In other areas, buyers can take their time to decide.

Given the times we’re living in, many wealthy American families are fleeing the cities for less densely populated areas to work remotely and spend more time with their families. The “new normal” may be that their choice location for a second home is just as likely to be near — rather than far from — their permanent residence.

Use a Construction Loan to Build Your Second Home

The pros and cons of owning a second home

Buying a second home can fulfill a lifelong dream or quickly become your worst nightmare — which is why you need to make a balanced, informed decision. The following points may help drive your choices.

Pros

-

If you choose to take out a mortgage, you can choose the best time to buy to take advantage of low interest rates and depressed prices that lock in the price of your second home.

-

You can stay in your second home for as long as you want, whenever you want. If you plan on living there for more than six months out of the year, you may want to establish residency to potentially reduce your state income taxes (Florida, for example, has no state income taxes).

-

You can host family and friends during peak season or holidays, or allow them to stay at your second home throughout the year.

-

Your second property could be a steady source of income, as online rental services can easily facilitate and manage renting out the home for weeks or months at a time when you’re not staying there.

-

If you choose to not use your property as rental income, you can furnish your second home to express your personal taste and lifestyle, leaving personal belongings in place when you leave the property (i.e., clothing, furniture, household items, sporting equipment, and a car).

-

Hopefully, your property will increase in value over time and provide a return on your investment when it’s time to sell.

-

You can take joy in the pride of ownership and the memories you will build year after year in a place you love.

Cons

-

You have little or no control over your principality’s assessment of your second property — rising real estate taxes have become a challenge for home buyers in some states.

-

Out-of-pocket expenses can be steep. Mortgage payments (if you did not pay cash for the property), residential and groundskeeping fees, association assessments, recreational dues, professional services fees, real estate taxes, insurance, utilities, maintenance, and continual upkeep are just some expenses to consider.

-

Travel costs to and from your permanent residence to your second home can be time consuming and expensive, long-term.

-

The potential return on your original investment may be diminished if you need or want to sell in a buyer’s market.

Your second home has a future, too

One of your most important considerations is the purpose of your second home. Do you want to buy a house that will one day become the place where you retire? Will family stays become a tradition and the legacy of the home pass on to your children? Are you buying the home as investment property to generate income now and hopefully sell at a profit later?

A second home as a family asset is very different from investment property. That difference can affect your taxes and the insurance coverage you’ll need. If you rent out your property part of the year to offset your expenses, there are different tax rules depending on how much you use the property for personal or rental use. There are many more considerations that you should explore with your accountant or advisor.

Run the numbers

Whether you decide to take out a mortgage or pay cash for your second home, an experienced banker can be invaluable in helping you understand the various costs and other options available to you.

For example, instead of liquidating assets or using cash for the purchase, investors often have the additional option of borrowing against their securities. With securities-based lending, you retain ownership of your investment while borrowing against the value of it. This common borrowing strategy gives you flexibility, a sense of control, and preserves emergency cash. Your banker can explain all options available to help you make the best decision for your unique financial situation.

Costs vary by location

Home purchasing costs can vary all across the board, depending on the region of the country where you’re planning to buy. For example, a second home in a developing leisure community an hour or two away from your permanent residence may be less expensive — and more desirable right now — than established vacation hot spots across the country. Additionally, closing costs can vary from state to state and city to city. These nuances could be a difference of a few hundred dollars to a few thousand dollars. Rely on an experienced real estate professional to help you crunch the numbers.

It’s a big decision

Remember, purchasing a second home is a big decision that should be made carefully and in the context of your total financial life. Commerce Trust can help you build a team of professionals, including a banker, tax advisor, real estate agent and advisor to help you navigate the process. Contact us today — we will listen to your concerns and discuss how these and other considerations fit into your plan’s financial goals. ![]()

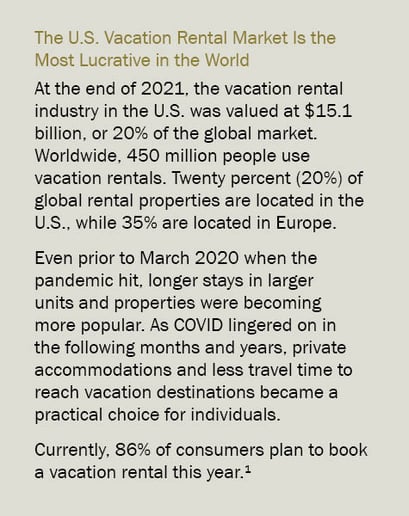

¹ipropertymanagement.com, “Vacation Rental Industry Statistics [2022]: Trends Pre- & Post-COVID,” https://ipropertymanagement.com/research/vacation-rental-industry-statistics, July 14, 2022.

Past performance is no guarantee of future results. The opinions and other information in the commentary are provided as of August 17, 2022. This summary is intended to provide general information only, and may be of value to the reader and audience.

This material is not a recommendation of any particular investment strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified attorney, tax advisor or investment professional. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax or legal advice, and may not be relied on as such.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed, and is subject to change.

The practice of lending, including lending involving marketable securities which are subject to changes in value, involves risk, including the risk of value decline or loss, and the risk of non-payment of lending obligations. Diversification does not guarantee a profit or protect against all risk. Securities-based borrowing exposes the borrower to unique risks. If the value of the underlying investments decreases sharply, the borrower may need to expedite repayment, or sell investments to meet the terms of a lending agreement.

Selling investment securities may result in adverse tax obligations. Commerce does not provide legal advice to customers. Commerce provides tax advice only to customers who have engaged Commerce to provide tax services. Consult a tax specialist regarding tax implications related to any product or specific financial situation.

Commerce Trust is a division of Commerce Bank.