Kevin Casteel, CFP® Trust Officer, Financial Planner

Kevin Casteel, CFP® Trust Officer, Financial Planner

For the most part, decisions about retirement are not made overnight. Whether you like it or not, retirement planning is a life-long process. That’s why it makes sense to have a good idea about what you want your retirement to look like before you determine how much you’ll need to save for the future lifestyle you envision.

It’s impossible to pinpoint an exact savings amount that will provide you with financial independence later in life — that’s because so many variables must be factored into the “secret formula.” But that’s just it — there’s no universal “secret formula,” no “magic number” for how much people need to save for retirement. Every person’s financial situation is unique, no two scenarios are identical.

However, you can arrive at a ballpark figure by applying the following percentages to your financial situation. Typically, you should plan on replacing anywhere from 75% to 90% of your income in retirement and account for multiple sources of retirement income. Saving and investing can fill a portion of the gap. The industry rule-of-thumb ranges from saving 10% to 20% of your income during your working years. While 10% savings seems a little low, 20% offers a strong start to retirement planning when split between pre-tax and after-tax savings.

Building a solid foundation for your retirement years early on allows for adjustments down the road as your plans and circumstances change. However, the estimated amount you need to save for your retirement depends in large part on your answers to the following questions.

What age do you plan to retire?

Traditionally, individuals retire around the age of 65. About one out of every three 65-year-olds today will live until at least age 90 — and one out of seven will live at least until age 95. Furthermore, married couples at age 65 today have at least a 50-50 chance that one spouse will live beyond age 90.² This means these individuals could be looking at a retirement period of between 25 and 30 years.

If you plan on retiring earlier, perhaps at the age of 55, you could have 40 or more years of expenses to cover — which means you’ll need to be more aggressive when it comes to saving and investing. As advances in medicine and the health care industry continue to improve, longevity estimates keep climbing. In fact, at the rate current life spans are increasing, you could spend more time in retirement than you spent working!

When did — or how will — you start saving?

The sooner you start saving, the quicker your money can get to work for you. Compound interest is key. The longer your money can grow, the more benefits it will provide you in the long run.

Keep in mind small steps can have a significant impact over a period of 30 or 40 years. That’s why it’s so important to start saving for retirement as soon as you can and maintain that habit over your lifetime. If retirement planning doesn’t begin until later in life, larger monthly or annual investment contributions may be needed to make up the difference — causing delayed retirement or financial distress. And, depending on your time horizon, the risk level and growth potential of your investments may vary.

How much have you already saved?

Take a look at the assets you already have earmarked for retirement. If you participate in a 401(k) plan, that’s a great start. Make sure you are aware of plan details and contribute enough to at least maximize the company contribution. Also, saving and investing outside of retirement plans adds flexibility and diversification for retirement spending.

Strive to put at least 10% of your compensation into savings. However, avoid relying solely on pre-tax savings to fund your entire retirement. Why? Because it will cost you $1.30 of pre-tax savings to get $1 after tax if you assume a 25% tax rate—so your $1.3 million pre-tax retirement account is really $1 million after tax.

In addition to saving in pre-tax accounts such as employer retirement plans or individual retirement accounts (IRAs), try to diversify your assets with regard to IRS tax guidelines and consider putting money in a Roth 401(k), Roth IRA, or an after-tax investment account. You’ll be glad you have the flexibility to fund your retirement from pre-tax and after-tax savings.

What additional sources of retirement income do you have available?

Don’t forget to account for retirement income outside of your investments. For example, retirees may receive payments from sources such as Social Security, pensions, trusts, or home equity.

For example, let’s say you want an after-tax retirement income of $10,000 per month ($120,000 annually). If you figure $48,000 or 40% will come from Social Security, you’ll have to fund the remaining $6,000 per month ($72,000 annually). This projected income would require $2 to $3 million in savings, depending on the tax characteristics and asset allocations. Your financial advisor can take a look at your individual situation and help you project how much money you will have from all your income sources when you retire.

What kind of lifestyle will your savings support?

To invest strategically for retirement, it’s important to have a good idea as to what your expenses will be once you arrive at that stage of your life. You should:

-

Have a clear understanding of the lifestyle you want to live and the budget it will take to maintain it.

-

Know where you want to live — perhaps you choose to move to a favorite place you’ve visited or to a lower-cost state or country with an attractive income tax rate or cost of living.

-

Decide what you want to do with all your time — perhaps start a second career, travel, take up a new hobby, or volunteer for your favorite charity.

-

Plan carefully for rising health care and insurance costs.

-

Think about inflation — goods and services are likely to cost more in the future.

We can help

Planning for retirement involves several variables — sometimes the process can be overwhelming. You can start by sharing your answers to the five questions in this article with a Commerce Trust advisor. Learn how we can create a retirement plan based on your unique financial situation to help you live the lifestyle you envision. Call today.

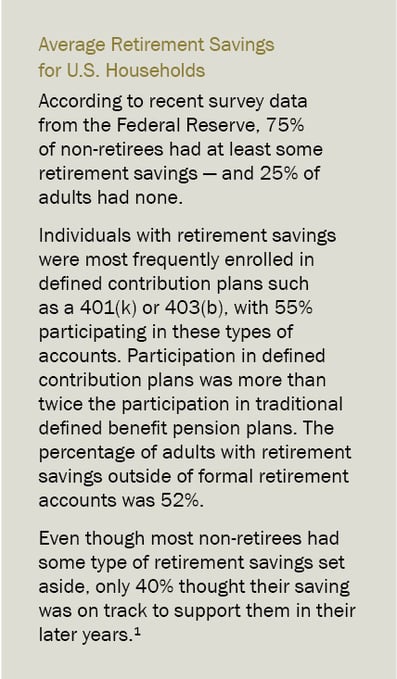

¹Federal Reserve, “Report on the Economic Well-Being of U.S. Households in 2021, https://www.federalreserve.gov/publications/files/2021-report-economic-well-being-us-households-202205.pdf , May 2022.

²SSA.gov, “When to Start Receiving Retirement Benefits,” Publication No. 05-10147, https://www.ssa.gov/pubs/EN-05-10147.pdf, January 2022.

The opinions and other information in the commentary are provided as of July 21, 2022. This summary is intended to provide general information only, and may be of value to the reader and audience.

Past Performance is not a guarantee of future results. Diversification does not guarantee a profit or protect against all risk.

This material is not a recommendation of any particular investment or insurance strategy, is not based on any particular financial situation or need, and is not intended to replace the advice of a qualified tax advisor or investment professional. Commerce does not provide tax advice or legal advice to customers. Consult a tax specialist regarding tax implications related to any product and specific financial situation. While Commerce may provide information or express opinions from time to time, such information or opinions are subject to change, are not offered as professional tax, insurance or legal advice, and may not be relied on as such.

Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Commerce Trust is a division of Commerce Bank.

Not FDIC Insured / May Lose Value / No Bank Guarantee